European Commissioner Lazlo Andor keynote speech at ETUI conference “Labour markets in the crisis”

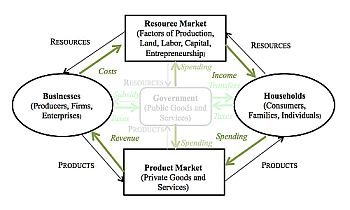

Product Markets: The Evidence

EMU in the end was a political decision. Economists around the world were more or less skeptical.

Their fundamental concern was an obvious lack of flexibility in the economies of potential member states, and as a consequence, in the future monetary union. For example, on February 9, 1998, 155 German academic economists published an open letter entitled “The Euro Is Coming Too Early”- the main reason being the lack of flexibility in labor markets (and insufficient progress in consolidating public finances).And it was in the first weeks after the establishment of the European Central Bank (ECB) when Milton Friedman saying, “Congratulations on an impossible job. You know I am convinced, monetary union in Europe is doomed to fail.” In short, a clear majority of economists pointed to the fact that a monetary union with the envisaged large membership-eleven countries finally to start on January 1, 1999-would be far from fulfilling the criteria of an optimal currency area (OCA). But, the project of monetary union, the ambition to be allowed to participate, and after entry, the need to adapt to the new framework of a single monetary policy-“one size fits all”-and the removal of the tool of national monetary policy and changes in the exchange rate of the national currency strengthened structural reforms and fiscal consolidation.

The conditions for entry enshrined in the Maastricht treaty-at least formally-referred only to nominal variables. The discipline exerted by these criteria in some cases came late, but all in all, it was timely enough. The threat of not being in at the start of EMU unleashed unexpected forces, including the sphere of fiscal policy-admittedly with grave exemptions as regards public debt levels.

But what about structural reforms, progress toward greater flexibility in product and labor markets? The authors identify two layers of a potential impact of EMU.

One is (dis)qualified by AAG as “wishful thinking”-the rhetoric that “any step toward integration is ‘by definition’ good and brings about all sorts of wonderful achievements for the continent.” Strange as it might sound for an economist, this “philosophy” of integration-or what it may be called-played for some time an important political role under the label of the “monetarist” position. This was based on the expectation that once the exchange rate was fixed irreversibly, the rest would adjust in a mysterious way.

The other line of argument refers to the fact that monetary union eliminates the option of strategic devaluations, or more generally of adjusting policy rates to national cyclical conditions, and therefore enforces pressure for enhancing the flexibility of labor markets and wage bargaining.

In this context, AAG mention that not surprisingly, the pre-euro debate initially focused on labor market reforms. The effect on product markets comes mainly from increasing costs of regulation due to stronger competition to what extent are the criteria of OCA endogenous? What is the impact of EMU on concrete steps for more flexibility in product and labor markets? Here, AAG are confronted with a tremendous identification problem. The authors concentrate their empirical study at a one- shot event-the introduction of the euro. The difficulties to isolate this effect from the rest of the environment are obvious-and fully recognized by the authors:

1. The process of globalization has created incentives for reforms worldwide.

2. The introduction of the euro is not just exogenous. Countries discussed pros and cons and adapted to the common currency for different reasons, which could have also affected incentives for structural reforms.

3. The effect of the introduction of the euro preceded the start of EMU.

As soon as it became a common conviction that EMU would begin as agreed in Maastricht on January 1, 1999, risk premia in foreign exchange markets started to decline, and preparation for participation reached a decisive phase.

4. The observation period still is rather short-further impact might be in the pipeline.

5. Finally, and most importantly: is it possible to disentangle the effect of participation in the single market from the introduction of the euro?

The main result of their empirical study can be summarized in two sentences:

1. The adoption of the euro had a significant effect in promoting the adoption of product market reform, especially in some sectors. Here, one is tempted to argue that the impact should rather be in general terms (i.e., comprise structural reforms on a broad macro level). So, are sectoral reforms more due to sectoral specifics than to the introduction of the euro?

2. For labor market reform, the euro did not have much of an effect. Here, one may caution a bit. For example, the euro may have contributed to the major labor market reforms that were implemented in Germany in 2004 and early 2005.

The authors are also convinced that the sequencing of reforms should follow this pattern.

I will not try to evaluate the statistical method applied, or to go through the myriad of details. While the data are impressive, it would help if the authors could try to consolidate their results.

The AAG chapter sets a landmark in extracting information from their model on an issue of highest importance for the functioning of EMU. Overall, their results are consistent with those of other studies. In the meantime, the European Commission has published its “EMU@10” special report (2008). Its summary concludes: The evidence is not very conclusive, but it is clear that on balance the single currency has had little positive effect on the pace of structural reform. Consistent with these findings, the analysis . . . indicates that euro- area countries have on average been less forthcoming in implementing the structural policy recommendations made to them by the EU under the Broad Economic Policy Guidelines (BEPGs)-a Treaty- based tool for economic policy coordination-in the period 2000-2005. In particular, progress in the cross- border integration of services has been more muted than expected, which is particularly problematic. It is in this area especially that price rigidities persist. This has been recognized by . . . the European Commission, which in turn has led to intensified surveillance of national structural policies in the euro area in the framework of the Lisbon Strategy for Growth and Jobs, which was revamped in 2005.

Where Is EMU Going?

Notwithstanding the remaining lack of flexibility, especially in labor markets, the single monetary policy has worked with great success-certainly better than even the optimists had expected. This result might trigger a new discussion on the relevance of the OCA criteria. Financial integration might have played a role. Consumption smoothing and risk sharing should have contributed to the functioning of EMU.

On the other hand, significant challenges are ahead. Countries that continuously have lost competitiveness inside the euro area are confronted with heavy adjustment problems, and the slowdown of growth will reveal the lack in ambition on structural reforms throughout the euro area. The costs of the current financial crisis for the real economy will to a large extent depend on the flexibility of labor and product markets-in particular, on (downward) flexibility of labor costs and prices. In my book The Birth of the Euro (2008), the title of the last chapter, “Europe at the Crossroads,” is a kind of short- cut message. The there- is- no- alternative (TINA) to structural reforms hypothesis remains true if the coherence of the area is to be preserved and the functioning of the single monetary policy guaranteed. The alternative is anything but promising: increasing tensions-economicallyand politically-with far-reaching consequences.

{kind=link}