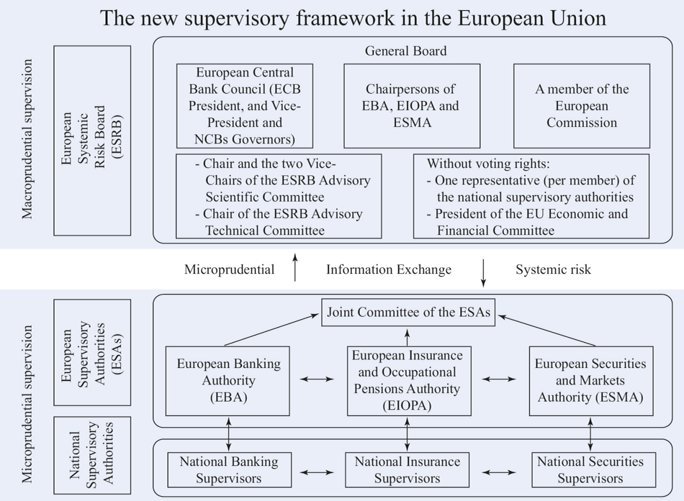

Reforming the euro and European financial architecture

Financial Architecture

Alternative models for reforming financial architecture in Europe will have profound implications for the degree of financial market integration, competitiveness in the financial industry, and financial and monetary stability.

Reform proposals should be assessed in terms of their contributions to the welfare of European citizens, including the price they will pay for financial and payment services, the range of opportunity for insurance and portfolio diversification, and the reliability and trust of the financial institutions in the area.

The financial architecture in Europe is clearly in a process of deep change. In its present shape, there are at least three significant problems. First, there are areas in which the present financial architecture arrangements are not adequate for financial stability. For instance, in the event of a crisis, there is no clear chain of command among the institutions potentially involved in any intervention. How would the euro system react to the threat of a major disruption like the one ensuing from the possible bankruptcy of Long Term Capital Management (LTCM) in the US in 1998?

Who in Europe would have the responsibility to organize a rescue of a large financial institution, as did the president of the Federal Reserve Bank of New York in the case of LTCM? A response based on improvised co-operation may not be enough – it may come too late. Moreover, there could be misaligned incentives for national supervisors dealing with transnational firms, leading to too little interventions, as they do not internalize cross-border spillovers from the crisis of such firms. Conversely, national authorities may have strong incentives to provide excessive help to national champions.

This view is in contrast to the conclusions of Brouwer’s reports (of March 2000 and April 2001)4 in the EU, according to which all these potential issues can be satisfactorily addressed with just a little bit more co-operation among supervisors in the various member states. Second, the present arrangements hinder European financial market integration to a large extent. Legislation is slow, rigid, and lags behind market developments. Regulatory fragmentation prevents the emergence of liquid European markets (as arguably was the case in the failure of the London Stock Exchange and the Deutsche Börse to create iX). Protection of national champions and regulatory barriers avert the emergence of pan-European banks.

Third, the present arrangements hinder the competitiveness of EU financial markets and institutions. There is considerable uncertainty about the normative and regulatory framework in Europe. Market fragmentation resulting from regulatory barriers slows down and distorts the emergence of cross-national firms that may be able to compete at international level. Until recently, the “official” view has been that this state of affairs is not worrisome because European banking and financial markets remain segmented. In a framework of segmented markets, all that is needed is more co-operations among different regulators and authorities.

This view may clearly backfire, as it justifies a slow pace of reforms and policies that do not remove obstacles to integration. Ultimately, this may just be a way to endanger stability. Many political-economy issues are at the heart of the problem, namely, the tension between economic integration and the lack of willingness to relinquish national political control. But while these political economy issues slow down the pace of regulatory and institutional innovations, there are important sources of systemic risk to which the European markets are exposed.

The recent events have stressed the threat of terrorist action, and possible financial weakness associated with economic slow-downs. Some European banks are heavily exposed to emerging markets and to particular sectors, such as telecoms, which have recently experienced deep crises. The process of consolidation within countries has led to the creation of many “national champions,” which may create incentives for national authorities to provide excessive guarantees. At the same time, the expansion of cross border activities may increase potential spillovers and externalities across countries, while creating incentives for under-provision of supervision and liquidity support by national authorities.

The present approach to reforms is gradualist, based partially on the so-called “cosmetology,” consisting in delegation of powers to define rules to various committees. This approach has its limits, and may yield more costs than benefits in the long term. It may be preferable not to wait for a major crisis to strike in order to put the house in order.

There is good reason to endorse in general the well-intentioned recommendations of the committees and groups seeking to remove the obstacles to European financial integration. Yet the question is whether a more ambitious approach would be more appropriate. In particular, what prevents the immediate setting of clear procedures for crisis lending and management with the European Central Bank at the centre?

Why not put a crisis framework in place now, and confront the fiscal issues related to the possible costs of intervention? By the same token, a debate should be opened with a view towards evaluating the benefits of more centralized supervisory arrangements in banking, insurance, and securities. In addition to the current decentralized regulatory competition framework, there are other long-run models that one could follow. In the first model, the ECB and ESCB might gain a larger role in supervision of banking, with the contemporaneous creation of separate specialized European-wide supervisors in securities and insurance.

The second model consists of an integrated supervisor for banking, insurance and securities, a European Financial Supervision Authority (EFSA), whereas the ECB would have access to supervisory information in order to maintain systemic stability. Different models present different trade-offs between efficiency, accountability, but also suitability to specific circumstances and features that may differentiate markets and financial institutions across regions. It may be important to note here that in neither of the two models above, supervision need be completely centralized at the European level.

First, national supervisors will need to be involved in day-to-day operations. Second, national institutions could still have the supervision of entities that trade mostly within one national jurisdiction (under the home-country principle).

The door should be left open in the Convention on the Future of Europe to the necessary institutional changes to implement more centralized regulation, perhaps along the lines of one of the models above. At the same time, the EU-wide competition policy in the banking sector should limit help to national champions (which are “too big to fail”), and remove obstacles to cross-border mergers. Domestic competition policy should also be reinforced, as to keep in check local market power.

Reforms of the financial architecture are admittedly quite complicated, as technical aspects are strictly interwoven with legal and institutional aspects. Given the large interests at stake, the process of reform is the target of particularly strong lobbies, both private and public. It would be a great cost for society if the need to reconcile conflicting special interests resulted in a lower protection of European citizens against the many risks that an inefficient and vulnerable financial system entails.

{kind=link}