“Neiter fortunes nor flowers last forever”

Chinese Proverb

VIDEO

The crisis in Europe: Structural reform necessary for survival

The Euro and Structural Reforms

Introduction

One of the arguments in favor of the introduction of the common currency area in Europe was that it would have pressured member countries to improve their macroeconomic policy and pursue “structural reforms,” the latter being defined as labor and product markets’ liberalization and deregulation.

Has it worked? Have members of the euro area had a better policy performance after adopting the common currency?

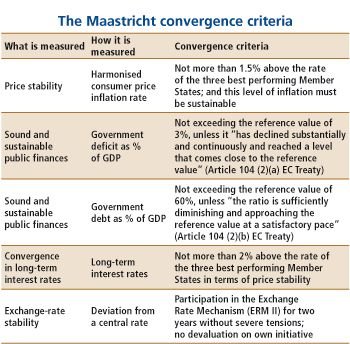

High-inflation countries have gained a sound monetary policy with the adoption of the common currency and the European Central Bank. The euro does not have any direct implication for fiscal policy, but its adoption was accompanied first by the imposition of converge criteria on budget deficits and public debt and then by the Stability and Growth Pact (SGP), which established some rules about deficits. For some high-debt countries (e.g., Italy, Belgium, and Greece), the threat of being left out served as an incentive to initiate fiscal adjustments. However, once the euro was introduced, the threat of exclusion vanished, large deficits reappeared in several member countries, and the SGP was widely violated.

Why should joining the common monetary area accelerate and facilitate structural reforms?

We can think of a few sound economic arguments and some wishful thinking. On the former (and more solid) ground, more competition due to the single market might increase the cost of regulation in the product markets. The protection of insider firms and workers would become more costly and more visible to consumers and voters. For example, imagine a country that protects a national airline at the expense of a low-cost one that flies in the rest of the union: the costs for the travelers and taxpayers would be large and obvious. This would also weaken the insiders of the protected national airline, from union workers to pilots to managers accumulating losses at the expenses of taxpayers. Of course, this argument presupposes that the euro per se is a necessary condition for having a truly common market, a point which requires discussion. Second, the elimination of strategic devaluations shuts down a (possibly temporary) adjustment channel for a country losing competitiveness. In the product market, this means that firms and their organizations may demand deregulation of the market for inputs such as no tradable services, energy, and transportation to contain costs. Also, if real wage growth is out of line with productivity, a nominal devaluation is not available any more as a solution (or a palliative). This creates incentives for countries to free their labor markets from regulations that create obstacles for real wage adjustments and labor mobility and flexibility. In fact, those who were skeptical about the introduction of the euro raised precisely the issue of real wage adjustment and labor market rigidities: the elimination of those was seen as a condition difficult to implement but necessary for the euro to survive. It is interesting to note that the pre- euro economic debate focused much more on labor market reforms and much less, or not at all, on product markets, while in reality, as we will see later, the latter markets were liberalized first.

The wishful thinking part was the rhetoric often too common in Europe, according to which any step toward integration is “by definition” good and brings about all sorts of wonderful achievements for the continent. More seriously, many commentators viewed the adoption of the euro as essentially a political move, a step toward some sort of United States of Europe. Jacques Delors is quoted as saying, “Obsession about budgetary constraints means that the people forget too often about the political objectives of the existence of unemployment benefits. This makes sense, as the deregulation of product markets implies labor reallocations across firms and sectors, which require some labor market flexibility; any may lead, at least in the short run, to higher unemployment.

We should be clear from the start that we are considering a handful of countries: eleven original members of the euro area (all but Luxembourg), a few EU but not euro members, and the remaining Organization for Economic Cooperation and Development (OECD) countries. We are also looking at a one- shot event: the introduction of the euro. It is possible that a certain timing of reforms across countries may lead to a spurious correlation that happens to coincide with the adoption of the euro.4 Or, it may be possible that it is not the euro per se but the membership in the European Union that creates incentives for product market deregulation, and there are simply not enough countries that are members of the European Union but not members of the monetary union to identify this difference.

Finally, the decision to adopt the euro is clearly not exogenous, and we try to address issues of endogeneity. The recent literature on currency areas (Alesina and Barro 2002; Alesina, Barro, and Tenreyro 2002) offers insight about instruments that may have led to the decision of adoption. One should be aware, however, that various countries adopted the euro for different reasons.

In some cases, it was done mostly for anchoring purposes (e.g., in Italy), while in other cases, the intention was to be at the core of the European integration process (e.g., in France and Germany). In fact, one theme of the pre- euro debate amongst economists was what is the benefit for Germany?

There seemed to be no big economic gains for this country, which seemed to provide the service of being an anti- inflation anchor without receiving an obvious benefit in return. However, the benefit was political. To put it differently, the decision was partly dictated by noneconomic factors, hard to capture with an instrument.

We are not the first to investigate the relationship between the adoption of the euro and structural reforms. The International Monetary Fund (2004) suggests that belonging to the European Union accelerates the reform process in the product market but has no conclusive effect on the labor market.

Yet, this paper fails to disentangle the effects of the adoption of the euro and of the European single market (ESM). Hoj et al. (2006) provide supporting evidence to these results. They find a positive effect of the ESM on product market reforms-particularly in the transportation and telecommunication sectors-but no impact on the labor market. However, they do not directly test for the effects of the euro. Duval and Elmeskov (2005) instead investigate this issue using a database of OECD countries in which they analyze large structural reforms in the labor and product market. Stacking together these (different) reform measures, they conclude that a lack of monetary autonomy, which is defined as belonging to the European Monetary Union (EMU) or to other fixed- exchange rate regimes, can have a negative, signify cant impact of the probability of undertaking large structural reforms, but only in large economies. In a database of 178 countries on a longer, yet less- recent, time span (1970 to 2000), Belke, Herz, and Vogel (2005) obtain different results. They find that a higher degree of monetary authority independence, as measured by an index of exchange rate flexibility, has a positive impact on an overall index of reform effort, especially in the financial and banking sectors. They find no robust evidence for an index of market regulation in the sample of OECD countries.

1. For instance, some directives of the European Commission regarding some sectors decided in the mid- 1990s implied actions to be taken in 1998 and 2000 for all members of the European Union. This timing coincided with the adoption of the euro. Note, however, that these directives do not apply only to EMU countries but to all the EU countries. Nevertheless, this timing may imply some spurious correlation.

2. For instance, Austria is classified under a de facto fixed-exchange regime with the deutschemark, even before the EMU.

{kind=link}